Karla Simon

As Chinese academics and the government seek to devise a system under the proposed ‘charity’ or public benefit law for adoption by the National People’s Congress in the coming years, the question of how ‘people’s organizations’ should qualify as being of public benefit (gongyi zuzhi) arises. In this post we will address that question.

In common parlance in China, qualification as a gongyi zuzhi is being designated as ‘certification’, and that term is used here. Certification follows the legal coming into existence of a minjian zuzhi or a local community organization, through either registration or ‘recognition’ (bei’an).

In countries around the world there are essentially two different processes used for ‘certification’, the commission model and the tax model. The commission model proceeds from the situation in England and Wales, where the Charity Commission makes such determinations, and has done so since 1601. The ‘tax model’ is exemplified by the Internal Revenue Service (IRS) in the US. Asian examples of both models are also available for China’s consideration.

In China, the commission model has been proposed by the China Philanthropy Research Institute (CPRI) in its draft ‘Charity Law’. One of the rationales for such a system can be found in CPRI’s reliance on the newly adopted (2006; effective 2008) Public Benefit Commission in Japan. While not perfectly emulating the Japanese system, CPRI’s proposal would largely adopt it. The PBC in Japan reports to the Prime Minister’s office, while the ‘Charity Commission’ in China would report to the State Council.

In contrast, the current system for ‘certification’ as a public benefit organization in China follows the ‘tax model’, as in Taiwan and Hong Kong. At the present time, the Ministry of Civil Affairs (MCA) and the State Administration of Taxation (SAT) cooperate in administering a set of clearly defined rules for qualification of both organizations and donations made to them. Thus, while CPRI’s idea may be a good one, it is unlikely that the entrenched bureaucracy would be in favour of it unless the new commission does not disturb its current role.

And that may well be possible, because instead of relying on prefectural (provincial-level) commissions to carry out local enforcement of nationally developed policies (as in Japan), CPRI’s draft would rely on the current MCA/SAT system. In a sense, then, the proposed CPRI model is a true hybrid. It relies on a high-level commission to set policy and establish procedures while at the same time allowing the existing bureaucratic structures to make the practical decisions.

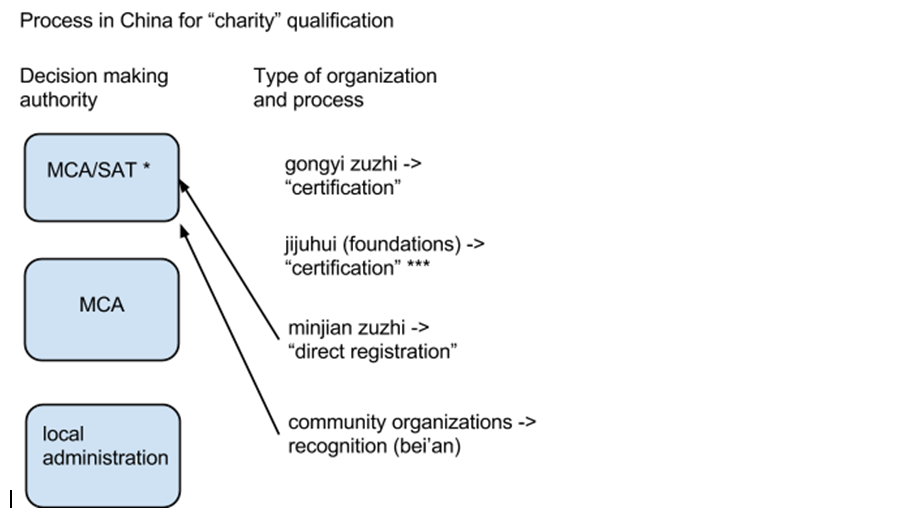

The following chart summarizes proposed procedures in China.

* The charity commission only makes policy and prescribes procedures; MCA and SAT administer them.

** Registered jijinhui must be for public benefit.

*** The lines clarify which organizations may apply to be ‘certified’.

Although this chart implies that all registered or recognized organizations may apply to be ‘certified’ as public benefit organizations, they may not all qualify. The next blog will consider what qualifications are necessary for such ‘certification’.

__________________________________________________________________________

Special note: The author has been engaged by the Asia Foundation to assist CPRI in the development of the Charity Law. Her commenting in this blog and elsewhere proceeds from that work.

Karla W Simon (西 门 雅) is chairperson of ICCSL

Comments (0)